Summary:

- Stand With Crypto UK has launched a campaign urging members to challenge banks that restrict transfers to cryptocurrency exchanges.

- The group argues that many blocked transactions involve exchanges registered with the UK's Financial Conduct Authority (FCA).

- A report from the UK Cryptoassets Business Council claims that roughly 40% of crypto transactions face restrictions or rejections from banks.

- One exchange reportedly saw nearly £1 billion in declined transactions over a one-year period due to bank-side restrictions.

- The campaign comes as UK regulators continue developing stablecoin and broader digital asset regulations.

- Advocates say banking access remains one of the biggest obstacles to crypto adoption despite the UK's ambition to become a global digital asset hub.

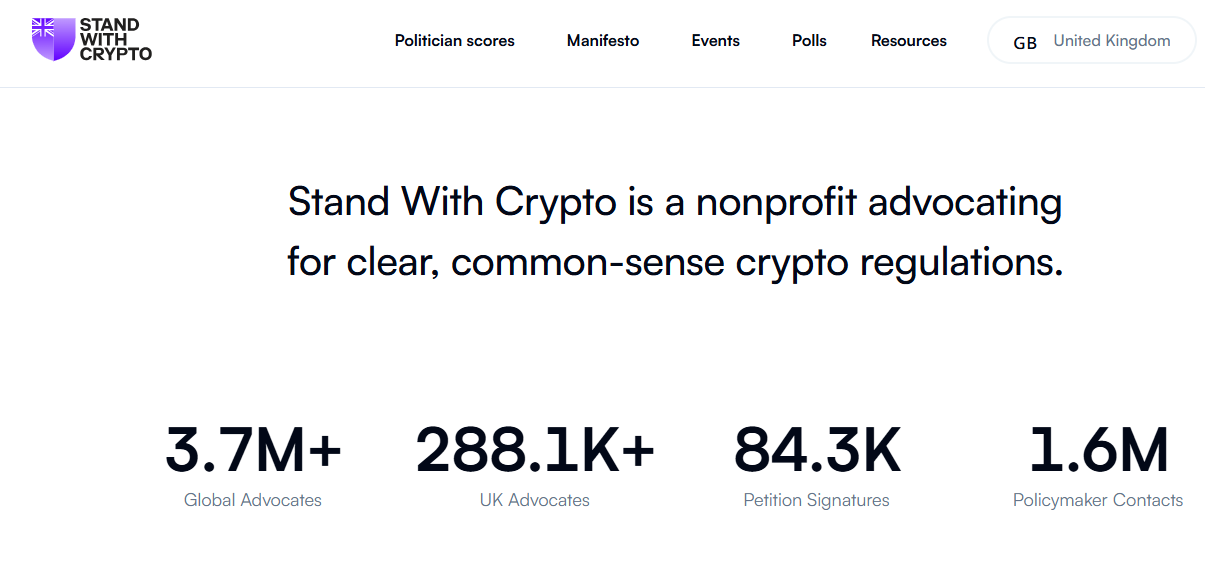

A growing dispute between the cryptocurrency industry and traditional banks is taking center stage in the United Kingdom, with advocacy group Stand With Crypto UK launching a new campaign aimed at challenging financial institutions that restrict customer transfers to crypto exchanges. The campaign arrives at a time when British policymakers are actively working on digital asset regulations and publicly discussing the country's ambition to become a leading center for blockchain innovation. Industry advocates argue that those ambitions are becoming harder to achieve when consumers continue to face barriers moving money between bank accounts and regulated crypto platforms. Stand With Crypto UK is now calling on its community to take action. According to the organization, more than 288,000 UK-based advocates are being encouraged to contact banks and policymakers over restrictions that they believe unfairly limit access to digital assets. The broader Stand With Crypto movement has grown significantly, reporting more than 3.7 million global advocates, over 84,000 petition signatures, and approximately 1.6 million policymaker contacts worldwide.

At the center of the campaign is a concern that many banks are applying broad restrictions to cryptocurrency-related transactions without adequately distinguishing between regulated exchanges and higher-risk activities. Supporters of the initiative argue that customers attempting to transfer funds to licensed platforms are increasingly encountering payment blocks, transfer limits, delays, or outright rejections despite using services that operate within existing regulatory frameworks. The campaign points to findings from a report produced by the UK Cryptoassets Business Council, which examined the relationship between banks and crypto businesses operating in the country. According to the report, approximately 40% of crypto-related transactions are either blocked or restricted by UK banks. The findings suggest that the issue extends beyond isolated incidents and may represent a broader challenge affecting both consumers and digital asset companies. The report also claims that one exchange experienced nearly £1 billion in declined transactions over a twelve-month period due to banking restrictions, while 80% of surveyed crypto platforms reported increases in blocked or limited transfers. Industry advocates argue that these restrictions create friction for users who are attempting to access regulated services while simultaneously sending mixed signals about the country's stance toward innovation. The debate has become increasingly important as digital assets move further into the financial mainstream.

Banking Access Remains a Major Challenge for Crypto Adoption

For many crypto companies operating in the UK, regulatory approval is only one part of the equation. Even when firms register with the Financial Conduct Authority and comply with anti-money laundering requirements, maintaining reliable access to banking services can remain difficult. Some platforms report challenges with payment processing, customer deposits, and banking partnerships despite operating within regulatory expectations. Banks often defend these restrictions by pointing to fraud risks and consumer protection concerns. Financial institutions have repeatedly warned that crypto-related scams remain a significant source of financial losses for consumers. In response, many banks have introduced transfer limits, enhanced verification procedures, or outright restrictions on payments involving cryptocurrency platforms.

From the banking industry's perspective, these measures are designed to reduce exposure to fraud and protect customers from potentially harmful activity. Crypto advocates, however, argue that broad restrictions can unintentionally affect legitimate users while limiting consumer choice. Industry groups argue that transfers to regulated exchanges should not automatically receive the same treatment as transactions involving unregulated entities or known fraud risks. They contend that customer-specific assessments would be more effective than blanket restrictions applied across entire categories of transactions. The issue has become particularly noticeable as digital asset regulation matures. Several major crypto firms operating in the UK now maintain registration with the FCA and follow compliance procedures similar to those expected of other financial businesses. Advocates argue that banking access should evolve alongside those regulatory developments. As governments develop rules for digital assets, questions increasingly extend beyond regulation itself and into how traditional financial institutions interact with the emerging sector.

READ MORE: Are Bitcoin Holders Selling for SpaceX? Onchain Data Suggests a Different Story

Stablecoin Policy and Digital Asset Reform Continue to Advance

The banking access debate comes as UK regulators continue shaping the next phase of the country's digital asset framework. Stablecoins have become a major focus for policymakers throughout 2026. In May, members of the House of Lords examined proposed stablecoin regulations and questioned industry participants about topics including anti-money laundering safeguards, financial stability concerns, and the potential impact on the traditional banking system. The discussions reflected growing interest in how stablecoins could fit into the broader financial landscape. Stablecoins are digital assets designed to maintain a stable value, typically by being backed by fiat currencies such as the US dollar or British pound. Supporters argue they could improve payments, settlement efficiency, and access to digital financial services. Regulators, meanwhile, remain focused on ensuring adequate safeguards are in place before widespread adoption occurs.

Later in May, the Bank of England signaled that it was reconsidering certain proposed restrictions involving stablecoin reserves and holding limits as part of its ongoing review of pound-denominated stablecoin rules. The discussion gained further momentum in June when a House of Lords committee warned that some proposed requirements could make pound-backed stablecoins less commercially viable. Lawmakers encouraged regulators to avoid measures that could unnecessarily limit growth while still addressing financial stability concerns. Beyond stablecoins, UK authorities have continued exploring broader digital asset reforms. The Bank of England has proposed extending operating hours for key settlement infrastructure, a move that could support tokenized financial markets and around-the-clock digital asset activity. Meanwhile, the Financial Conduct Authority proposed allowing certain retail-focused investment funds to allocate up to 10% of their portfolios to crypto exchange-traded products, marking another sign that digital assets are becoming part of mainstream financial discussions. The backdrop to these debates is a rapidly growing stablecoin market.

According to DefiLlama data, the total stablecoin market capitalization currently stands at approximately $316 billion. Against that backdrop, crypto advocates argue that banking access deserves greater attention. While policymakers continue discussing frameworks for stablecoins, tokenized assets, and digital investment products, industry participants say everyday users still face obstacles when attempting to move money between traditional banks and regulated crypto services. The campaign launched by Stand With Crypto UK highlights that disconnect. As the UK continues developing its digital asset strategy, the outcome of that debate may play an important role in determining how welcoming the country ultimately becomes for crypto businesses and users alike.

READ MORE: EU Targets Crypto in New Russia Sanctions Package, Proposes Ban on 11 Digital Asset Platforms