Summary:

- Two independent bitcoin miners each mined a full block this week, earning roughly $300,000 per block.

- Solo mining is extremely rare today, as most hash power is controlled by large mining pools.

- The wins highlight bitcoin’s probabilistic nature, where even small operators can still get lucky.

- The events come as U.S. mining dominance shows signs of softening, with other regions regaining share.

Bitcoin mining is often described as an industrial game now, dominated by large pools, warehouses full of machines, and massive energy contracts. That’s why this week stood out. Two solo bitcoin miners, operating independently, each mined a full block and collected the entire block reward. At current prices, that payout was worth roughly $300,000 per miner. It’s the kind of outcome most small miners never experience, and one that serves as a reminder that bitcoin’s rules haven’t changed, even if the odds feel stacked.

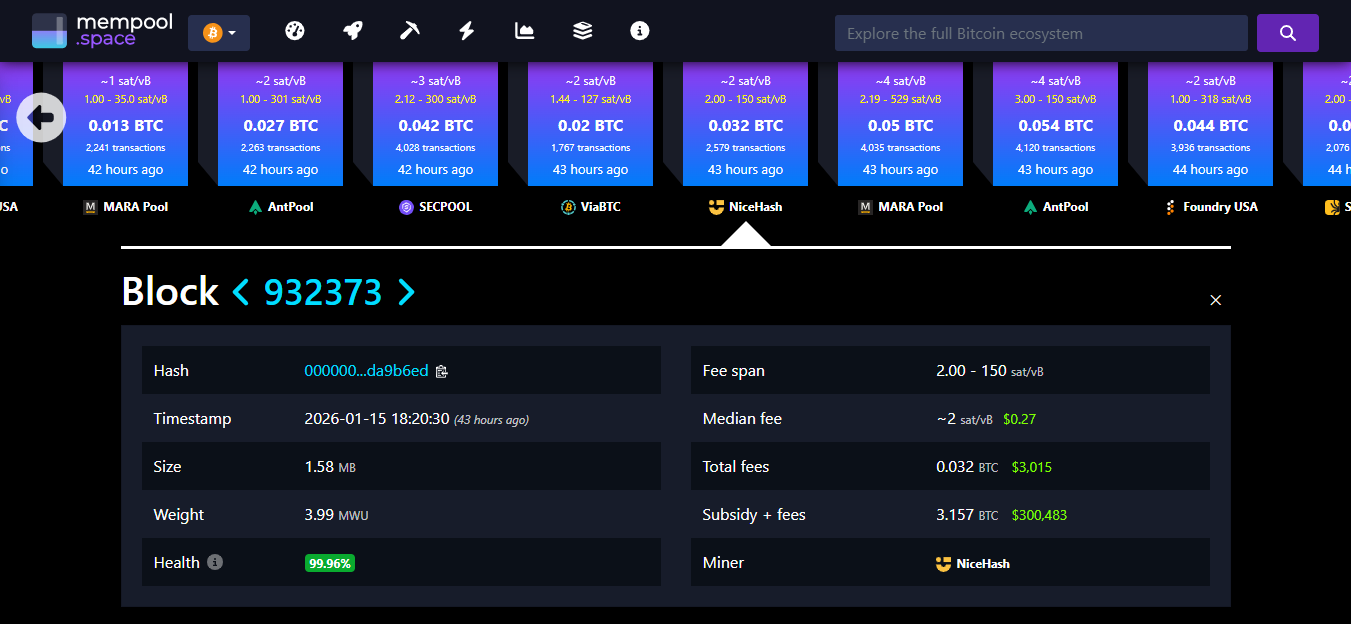

One of the blocks was mined early Thursday, according to public blockchain data. The miner earned a payout of 3.157 BTC, including transaction fees, after successfully producing block

Earlier in the same week, another solo miner found a block and earned a similar reward, valued at just under $295,000 at the time. That block can be viewed here

For most participants in today’s bitcoin network, outcomes like this are close to mythical.

Why solo wins are so rare

Bitcoin mining works on probability. Every miner is competing to solve the next block, and the more computing power you control, the higher your chances. But higher chances do not mean guarantees. Because the network has grown so large, most miners no longer mine alone. Instead, they join mining pools. These pools combine computing power from thousands of miners and distribute rewards proportionally. The trade-off is simple. You give up the chance at a massive payday in exchange for smaller, more predictable earnings.

Solo miners don’t get that stability. They might run hardware for months, or even years, without finding a block. But when they do succeed, they receive the full block subsidy plus transaction fees, with no pool operator taking a cut.That’s what happened this week, twice.

Data from mempool trackers shows that the vast majority of bitcoin blocks are produced by a small group of dominant pools. Foundry USA, AntPool, and F2Pool regularly account for a significant share of total block production, leaving little room for smaller or independent operators to win consistently.

Against that backdrop, two solo blocks in a single week stands out as a statistical outlier.

Luck still matters in bitcoin mining

These wins don’t mean solo mining has suddenly become practical for most people. The economics are still brutal. Electricity costs, hardware depreciation, and rising network difficulty make it extremely hard for small miners to compete. What these blocks do highlight is something more fundamental. Bitcoin mining is probabilistic, not deterministic.

Adding more machines improves your odds over time, but it does not control when the next block is found. That uncertainty is built into the system by design. Even the largest mining pools cannot predict exactly when they will mine their next block. And once in a while, that randomness favors a small participant instead of an industrial giant.

For solo miners, that randomness is the entire gamble.

What this means for small miners

For most people considering bitcoin mining today, joining a pool remains the only realistic option. Solo mining is still a long-shot strategy, closer to buying a lottery ticket than running a stable business. But stories like this week’s back-to-back wins keep the idea alive. They show that the protocol still treats every valid hash attempt equally, regardless of who produces it.

In a system increasingly shaped by scale and efficiency, that principle still matters. And every rare solo block reinforces the idea that bitcoin, at its core, remains open to anyone willing to take the risk. For two miners this week, that risk paid off in a very big way.