Summary:

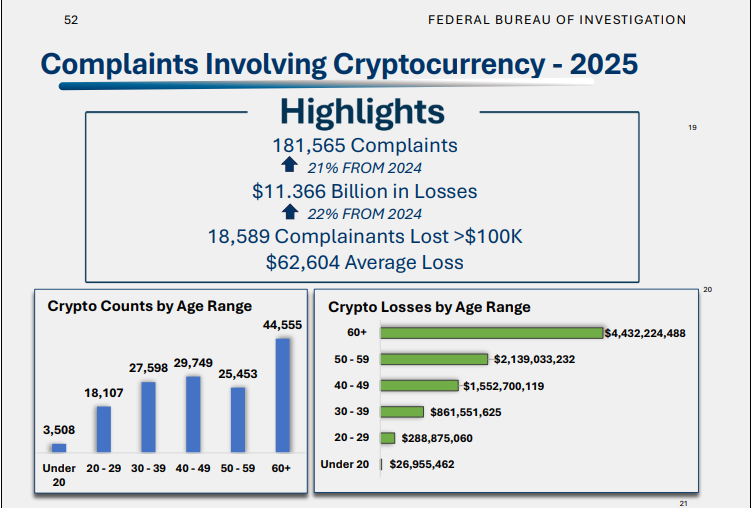

- Americans reported more than $11 billion in crypto-related scam losses in 2025

- The FBI received 181,565 crypto-related complaints during the year

- Investment scams remained the largest source of losses

- More than $5 million in losses came from complaints involving minors tied to crypto or crypto ATMs

- Government impersonation scams and fake FBI-themed crypto schemes also added to the threat landscape

The scale of crypto-related fraud in the United States continued to climb in 2025, with the Federal Bureau of Investigation reporting more than $11 billion in losses tied to cryptocurrency scams. According to the bureau's latest internet crime report, Americans submitted 181,565 complaints involving cryptocurrency during the year. Those complaints accounted for one of the largest categories of financial harm across all cyber-enabled crime. The broader picture is even larger. The FBI said it received more than one million cybercrime complaints in 2025, with total reported losses nearing $21 billion. Crypto and AI-linked scams stood out among the most expensive categories.

Investment fraud remained the main driver. The FBI noted that victims of investment scams were more likely to report paying in crypto than in cash, gift cards, debit cards, or other forms of payment. That pattern has become familiar. Crypto remains attractive to scammers because transfers are fast, global, and often difficult to reverse once sent. The FBI has tried to slow that trend through efforts like Operation Level Up, a program designed to identify and contact people who appear to be in the middle of active crypto investment scams. The agency says the initiative has helped reduce losses, but the latest numbers show the problem is still growing.

Minor Victims Were Also Affected

One of the more striking details in the report involves younger victims. The FBI said roughly 10% of the 13,168 cybercrime complaints involving victims aged 17 and under were tied to crypto or crypto ATMs. Those cases led to more than $5 million in reported losses. While that figure is small compared to the broader $11 billion total, it points to how crypto-related fraud is reaching younger age groups as well. The report does not break down each scheme in detail, but crypto ATM scams often involve fraudsters convincing victims to deposit funds into machines under false pretenses. In many cases, victims are told they are protecting their money, paying fees, or helping with an urgent issue. The data suggests that scam exposure is no longer limited to experienced investors or older retail users. It is spreading across a wider demographic.

At the same time, older Americans still remain among the hardest hit overall, with the FBI noting that people over 60 accounted for a major share of total cyber-enabled losses. Beyond fake investment platforms, impersonation scams also remained a major issue. The FBI recorded 32,424 complaints involving fraudsters pretending to be government officials, with those schemes causing around $800 million in losses. Some scammers even attempted to use the FBI's own branding as part of the fraud. Earlier this year, users on the Tron network reported receiving a token using the FBI logo and claiming their wallets were "under investigation." Victims were then prompted to submit personal information through what appeared to be an anti-money-laundering verification process. The message warned users that failure to comply could result in frozen funds. While the bureau referenced impersonation scams broadly in its report, it did not specifically mention that Tron-based scheme in the filing. Still, the example shows how scam tactics are evolving.

READ MORE: Bitrefill Hack Linked to Lazarus Group: 18,500 Records Exposed and Hot Wallets Drained

Crypto Crime Remains a Wider Global Issue

The FBI's report focuses on U.S. victims, but separate industry data suggests the global picture is even broader. Blockchain analytics firm Chainalysis estimated that illicit crypto addresses received at least $154 billion in 2025, with sanctions evasion and state-linked activity contributing heavily to that figure. That number includes more than consumer scams, but it shows how large the wider illicit crypto economy has become. For regulators and law enforcement, the challenge is no longer just about isolated fraud cases. It is about keeping pace with an ecosystem where scams, laundering, impersonation, and cross-border movement of funds can happen quickly and at scale.

Closing Thoughts

The FBI's latest report reinforces something the industry already knows but still struggles to solve. Despite more public awareness, improved analytics tools, and law enforcement initiatives, fraud losses continue to rise. Scammers are adjusting faster, using new tools, new narratives, and now increasingly AI-generated content to make schemes look more convincing. For the crypto industry, the numbers also carry a reputation cost.

Every billion lost to fraud becomes another data point critics use against broader adoption. And while most blockchain activity remains legitimate, consumer-facing scams continue to shape public perception.

READ MORE: Trump Cyber Strategy Puts Crypto and Blockchain Security at Center of U.S. Tech Leadership